Federal Solar Tax Credit Changes: Why Early Action Matters for Affordable Housing Developers

If your organization is considering adding solar on your multifamily affordable rental housing properties, now is the time to act. Recent federal legislation has changed how renewable energy investment tax credits work, introducing tighter timelines, new eligibility requirements, and added compliance considerations that are critical to determine if your properties can still qualify for these tax credits.

What’s Changed at the Federal Level?

HR1 was signed into law on July 4, 2025 and made major changes to the Investment Tax Credit (ITC) for clean energy projects under Section 48E. While the rules are complex, the key takeaway is simple: time is of the essence for affordable housing providers to take advantage of renewable energy tax credits for solar projects.

The following is a summary of key points contained in a more detailed guide prepared by Novogradac and Company for the Solar on Multifamily Affordable Housing (SOMAH) Program , which is available here.

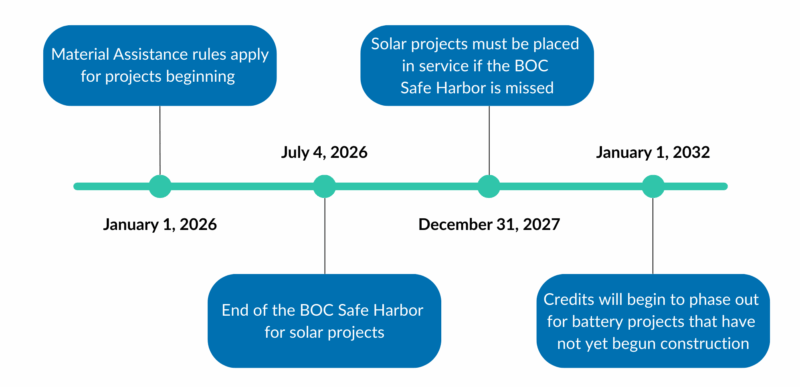

To qualify for the ITC, solar projects must either:

- Begin construction no later than July 4, 2026, or

- Be placed in service no later than December 31, 2027

Projects that begin construction by July 4, 2026 can take advantage of the IRS’s four-year Continuity Safe Harbor policy, which provides additional time to complete and interconnect the solar system.

- Note: Placed in service generally refers to the utility permission-to-operate date, not when the installation is complete. Permission to operate is granted after the solar system has been constructed and has passed all required city or county inspections. Prior to construction, an interconnection application is submitted and approved by the utility. After construction, the system owner submits final documentation, including the proof of passed inspections, as-built system diagrams, and executed utility agreements. The utility conducts a final verification and, upon approval, issues an official permission to operate notice.

- Example: If a project begins construction by February 1, 2026, it would have until February 1, 2031 to be placed in service under the Continuity Safe Harbor policy.

For projects that begin construction after July 4, 2026, the rules are stricter:

- The solar project must be fully complete and placed in service by December 31, 2027 to qualify.

Source: “How the One Big Beautiful Bill Act Changes the ITC” PDF. Prepared by the Solar on Multifamily Affordable Housing (SOMAH) Program and Novogradac and Company.

Bonus Credits Are Still Available for a Limited Time

Affordable housing providers may still be able to leverage the Low-Income Communities Bonus Credit (LICB) in 2026 while it’s still available. The future of the bonus credits beyond 2026 is uncertain.

- Provides an additional 10-20% adder for qualifying projects in underserved communities.

- 2026 application window opens February 2, 2026 with a 30-day priority period closing March 3, 2026.

- Note: This is a competitive process with only 1.8 gigawatts (GW) of capacity available nationally per round. Applying for this bonus credit adder requires a separate application process with additional details available on LICB website.

Good News for Battery Storage

While solar projects face tighter deadlines and restrictions, battery energy storage systems are not subject to the same beginning of construction or placed in service deadlines.

- Storage projects can still qualify for tax credits through 2032.

- FEOC restrictions do apply to storage projects.

Additional Project Size and Supply Chain Considerations

There are additional updates and considerations related to larger solar projects and new supply chain requirements that may affect eligibility and compliance. While these new rules introduce more complexity, particularly for projects over 1.5 megawatt (MW) AC and under the new Foreign Entity of Concern (FEOC) framework, the Partnership is well positioned to help navigate these requirements and provide assistance for your portfolio.

Why Affordable Housing Providers Should Still Pay Attention

Even non-profit developers who historically could not claim tax credits directly have two important reasons to stay engaged:

- Your organization may qualify for Direct Pay, which lets nonprofits and public agencies receive the tax credit value as a direct payment instead of a tax reduction.

- Your solar developer or investor can leverage the tax credits on your behalf. The ITC allows investors to claim the credits and pass savings along to the solar project, which can significantly reduce upfront costs or ongoing payments.

Organizations should consult tax and/or financial professionals to determine the best approach for their portfolio.

California’s Solar Incentives Remain Strong

Despite federal cutbacks, California’s state solar incentive programs continue to offer significant support to multifamily rental affordable housing. These programs can significantly reduce out-of-pocket costs, regardless of what happens with the federal tax credit:

Existing Buildings

- Solar on Multifamily Affordable Housing (SOMAH). Incentives for solar and integrated storage.

- Low-Income Weatherization Program (LIWP). Incentives for electrification upgrades, energy efficiency improvements, and solar.

New Construction

- Building Initiative for Low-Emissions Development (BUILD). Incentives for all-electric technologies and infrastructure, solar, storage, EV charging.

While these are the state programs the California Housing Partnership helps to administer, additional incentives may also be available depending on project scope and locations. Connecting with the Partnership as early as possible will help get you on the path to maximizing available tax credits and incentives while they are still available. Even if your organization is still in the exploratory stage, starting the conversation now can help clarify which properties may qualify, what timelines apply, and the steps needed to keep solar options open.

Connect with the Partnership’s Sustainability Team to get started.